Understanding the Basics of Social Security and Medicare (2024)

Social Security and Medicare can often feel overwhelming, with various rules, eligibility criteria, and strategic considerations influencing one's retirement planning. In this blog post, we dive into the essential aspects of these pivotal programs, offering detailed insights to help you make informed decisions. From understanding how benefits are calculated and the impact of taxes, to exploring claiming strategies and the nuances of spousal and survivor benefits, each section is designed to shed light on a specific area of Social Security and Medicare.

Whether you're approaching retirement or planning for the future, the information below provides valuable knowledge to guide you through the maze of options and regulations, ensuring you're well-prepared to maximize your benefits and secure a stable financial future.

- Eligibility and Earnings for Social Security Benefits

To be eligible for Social Security retirement benefits, individuals need to accumulate 40 quarters of work, equivalent to 10 years of employment. The benefits calculation takes into account the 35 highest-earning years of an individual's career. If there are fewer than 35 years of earnings, "zero years" will be averaged into the calculation, potentially lowering the benefit amount. For 2024, earning $1,730 grants one Social Security credit, with a maximum of four credits obtainable per year. This mechanism ensures benefits reflect an individual’s lifetime earnings, aiming to provide a safety net in retirement.

- Taxable Earnings and Benefits

Social Security taxes apply to earnings up to a maximum limit, which is $168,600 in 2024. There's no cap on earnings subject to Medicare tax. The maximum monthly Social Security benefit at full retirement age (FRA) is $3,822 in 2024. Both employees and employers contribute to Social Security and Medicare taxes, with self-employed individuals paying both shares, totaling 15.30%. Understanding these limits is important for financial planning, as they influence the amount of taxes paid and the potential benefits received.

- Understanding the Cost-of-Living Adjustment (COLA)

The COLA for 2024 is set at 3.2%, reflecting adjustments for inflation to maintain the purchasing power of Social Security benefits. This adjustment affects all retired workers, couples, and widowed beneficiaries, ensuring that their income keeps pace with rising costs. For example, the average benefit for retired workers before the COLA is $1,848, increasing to $1,907 after the adjustment. The COLA is an important feature of the Social Security system, designed to protect beneficiaries from the eroding effects of inflation.

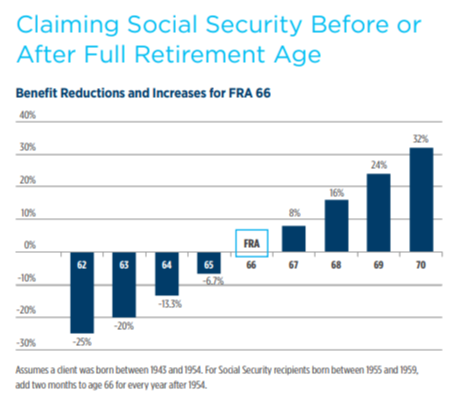

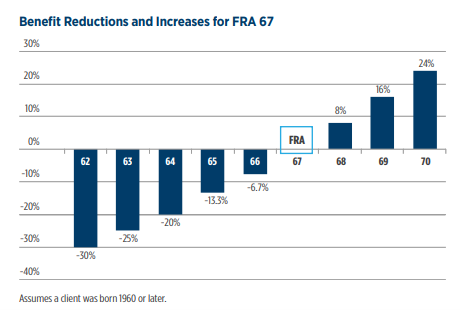

- Early Retirement and Earnings Reductions

Claiming Social Security benefits before reaching full retirement age (FRA) results in permanently reduced benefits. Additionally, if you work while receiving benefits before FRA, your benefits may be further reduced if your earnings exceed certain limits. For instance, in 2024, retirees under FRA can earn up to $22,320 without penalty, but above this limit, $1 is deducted from benefits for every $2 earned. Understanding these rules is essential for those considering early retirement or continuing to work while receiving Social Security.

Source: Social Security Administration (www.ssa.gov)

- Claiming Strategies for Social Security Benefits

Deciding when to claim Social Security benefits is a significant financial decision. Claiming before FRA results in reduced benefits, while delaying beyond FRA can increase benefits up to age 70. Strategies such as "file and suspend" or claiming spousal benefits require careful consideration of both timing and financial impact. Married couples, in particular, have several options to maximize their combined benefits, emphasizing the need for strategic planning based on individual circumstances and goals.

- Spousal and Survivor Benefits

Social Security provides spousal and survivor benefits, offering financial support to spouses and family members of beneficiaries. Spousal benefits allow one to receive up to 50% of the worker's FRA benefit, while survivor benefits provide up to 100% of the deceased worker's benefit to their widow(er). These benefits are subject to various rules based on the age of claiming and marital status, highlighting the importance of understanding Social Security's provisions for family benefits.

- Impact of Government Pensions on Social Security

Individuals who have worked in jobs not covered by Social Security, such as certain government positions, may see their benefits affected by the Windfall Elimination Provision (WEP) or Government Pension Offset (GPO). These provisions can reduce Social Security benefits to account for pensions earned in non-covered employment, aiming to balance benefits fairly among all workers regardless of the specific retirement systems they've contributed to.

- Medicare: Taxes, Premiums, and Coordination with Social Security

Medicare taxes are withheld from earnings regardless of income level, with additional taxes applied to higher earners. Understanding Medicare premiums is also vital, as they can vary based on income and affect one's overall retirement budget. Coordination between Medicare and Social Security includes provisions like the "hold harmless" rule, which protects Social Security beneficiaries from significant increases in Part B premiums, illustrating the interconnectedness of these federal programs in retirement planning.

- Additional Considerations: Earnings Tests, Marriage Requirements, and Important Ages

Social Security encompasses various rules, including earnings tests that determine how work income affects benefits and specific marriage requirements for spousal and survivor benefits eligibility. Additionally, understanding key ages for retirement planning, such as the earliest age to claim Social Security (62) and the age for required minimum distributions (RMDs) from retirement accounts, is crucial for comprehensive retirement strategy.

Each of these areas provides a piece of the puzzle in navigating the complexities of Social Security and Medicare, highlighting the importance of informed decision-making in retirement planning.

Mark J. Modzeleski, CFS, CLTC, AIF

President, Legacy Wealth Advisors of NY

Sources: Social Security Administration (www.ssa.gov), AMUNDI investment Management: Social Security 2024 Benefits Client Pocket Guide (2024 Amundi Social Security Pocket Guide.pdf)